BlackRock Touts Its “Green” Investments — While Working to Undermine Climate Regulations

Asset manager BlackRock has worked hard to build a reputation for prioritizing climate-friendly investments. But the firm is actively trying to take the teeth out of regulations that require companies to disclose their carbon emissions.

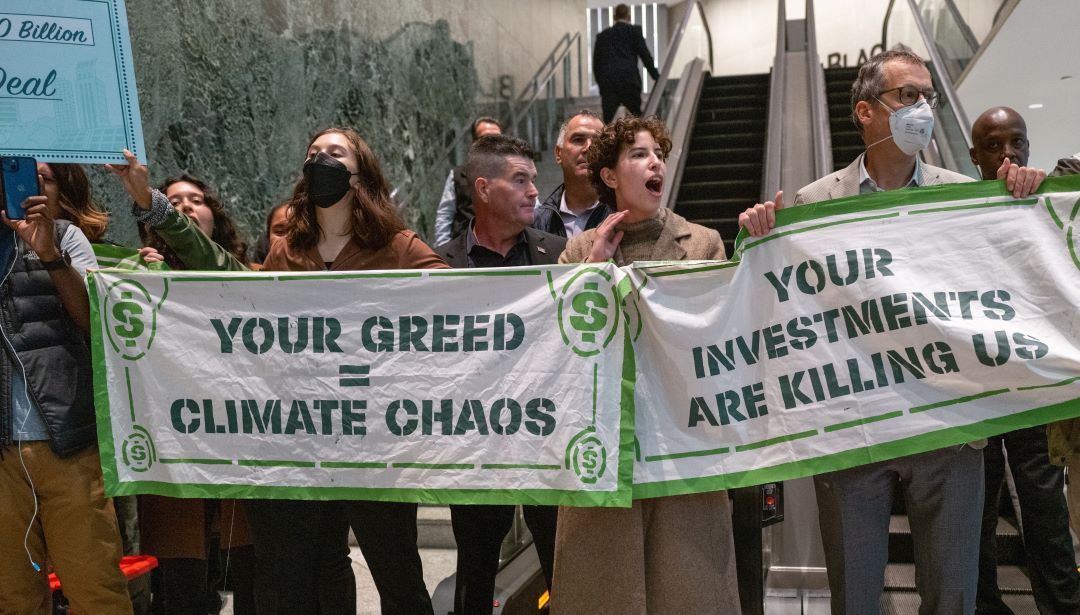

Climate activists block an escalator and throw coal on the ground at the New York headquarters of the financial investment firm BlackRock on October 26, 2022, in New York City. (Spencer Platt / Getty Images)

BlackRock, the world’s largest investment company, has become a top target of the Right’s crusade against so-called “woke capitalism” because of its rhetoric around climate change and sustainable investing. But when it comes to climate action, the giant asset manager isn’t presently all that far apart from its GOP detractors. Both BlackRock and congressional Republicans are fighting — albeit through different strategies — to defang a forthcoming regulation that would force companies to disclose their carbon emissions and the risks that climate change pose to their business models.

BlackRock CEO Larry Fink has warned that climate risk constitutes an investment risk. But after the Securities and Exchange Commission (SEC) proposed mandatory disclosure of those risks this spring, the $10-trillion asset manager is lobbying to weaken the final rule, according to our review of BlackRock’s rulemaking comments, federal lobbying disclosures, and meeting memoranda from the SEC. So far this year, the investment firm reported spending nearly $2 million lobbying on finance issues that include climate risk and environmental, social, and governance (ESG) disclosure.

The Wall Street Journal has described BlackRock as “walking a political tightrope” between activists on both sides of the sustainable investing debate. But the investment firm’s apparent attempt to undercut the type of measures it’s championed publicly for years instead suggests that it may have hit upon a more effective strategy for navigating the climate transition than the GOP’s outright denial. By aggressively growing the market for ESG funds — which typically net them higher management fees — while pushing watered-down regulations and maintaining its status as one of world’s largest fossil fuel investors, BlackRock can ensure that the climate crisis is a win-win-win.