How the First Black Bank Was Looted

In the early days of the Gilded Age’s rush for profit, freed people’s savings were siphoned off by politically connected financiers. Justene Hill Edwards’s Savings and Trust uncovers how finance cloaked dispossession in the language of uplift.

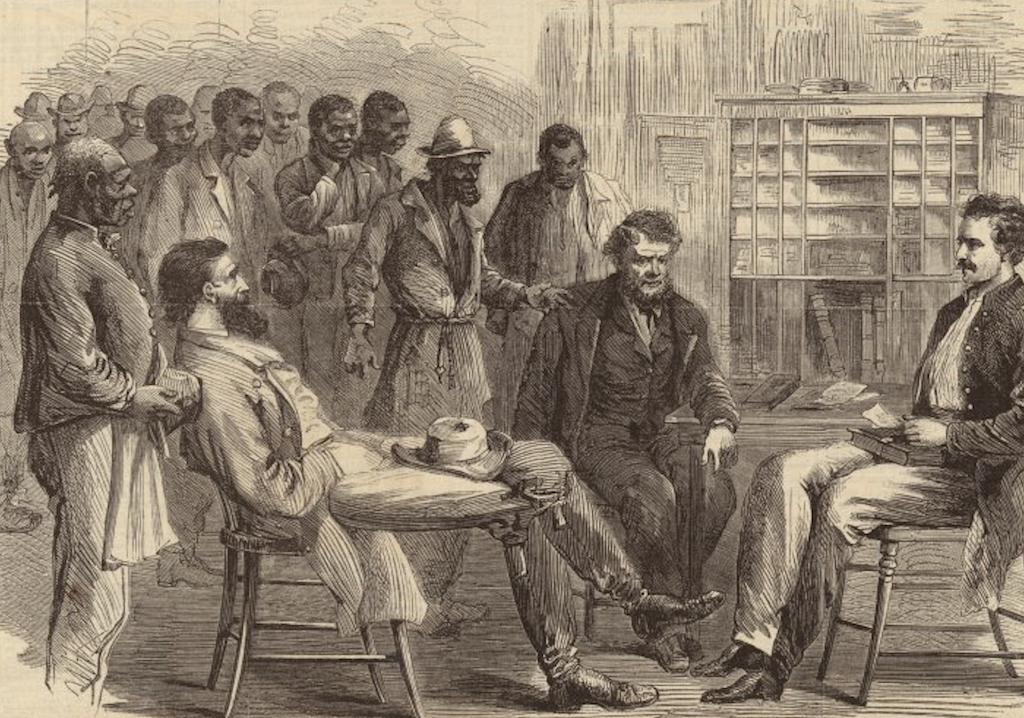

Etching of the Office of the Freedmen’s Bureau, Memphis, Tennessee, founded in 1865. (US Department of the Treasury)

Among the myriad metrics of inequality today, none appear so quintessentially American as the racial wealth gap. Today white households hold approximately 85 percent of all wealth in the United States whereas black families claim less than 4 percent. The median black family owns just 2 percent of the wealth of their white counterparts. Public-facing scholarship in recent years has sought to uncover not only the extent of such inequality in American life but the historical roots of it.

It is impossible to tell the story of the racial wealth gap, and indeed the story of the United States, without a full accounting of the history of enslavement and its long aftermath. Reconstruction was a revolutionary period of black political advancement and democratic possibility. But alongside its gains came a brutal backlash. In the South and beyond, black Americans were targeted not only physically but financially.

That Reconstruction was toppled by reactionary forces seeking to reestablish white supremacy in the South is well known. Less well known is how freed people’s northern Republican allies betrayed four million former slaves in the party’s quest to maintain political power and grow American capitalism. That story involves not simply abandonment but, before that, complicity — even entrapment — and contains within it an unlikely fountainhead of America’s racial wealth gap: the Freedman’s Bank.