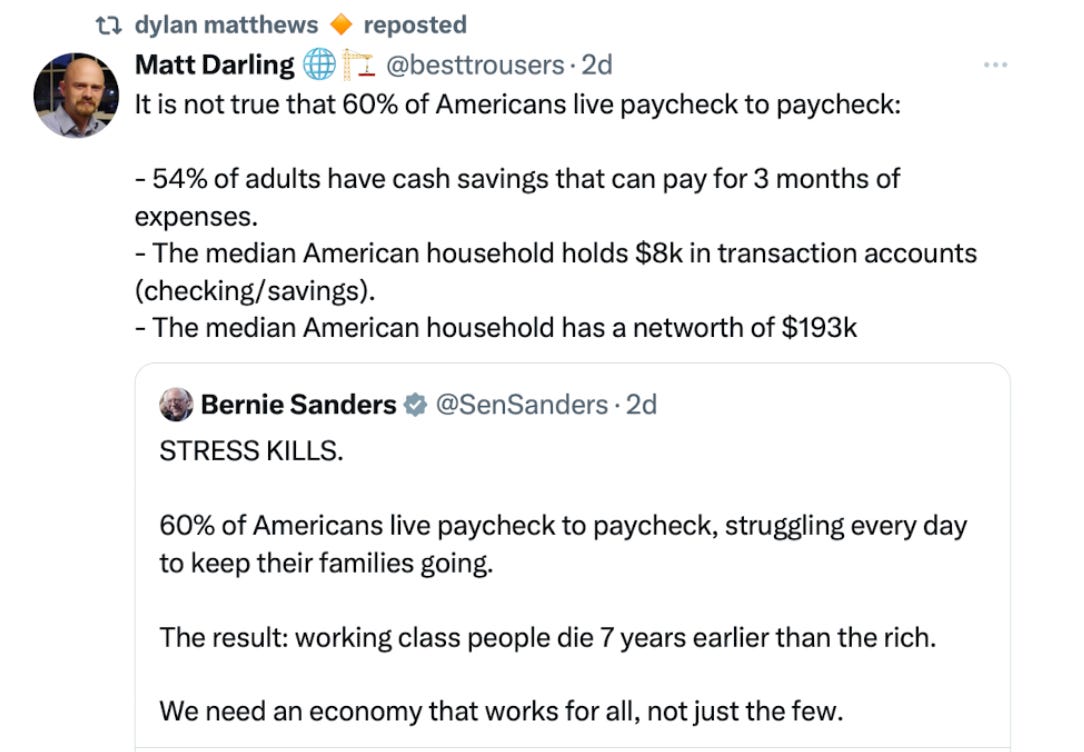

Bernie Is Right: 60% of Americans Live Paycheck to Paycheck

Bernie Sanders says it over and over again: 60% of Americans live paycheck to paycheck. Centrist critics swear this is false. Once we sort through the noise, we see Bernie is right on the money.

Bernie Sanders speaks to a capacity crowd during an event at University of Wisconsin–Parkside on March 7, 2025, in Kenosha, Wisconsin. (Scott Olson / Getty Images)

Bernie Sanders says it over and over again: 60% of Americans live paycheck to paycheck. But Matt Darling, formerly of the Niskanen Center, swears it’s not true, and Dylan Matthews of Vox calls it a damned lie. Even Matt Yglesias is apparently on the case, but I’m blocked from seeing his posts.

Who’s right and who’s wrong? Who should we listen to? Bernie Sanders — a model citizen of our community? Or the infamous Vox-Niskanen syndicate?