Wealth Increases Under Joe Biden Haven’t Meant Much for Most People

Some have defended Joe Biden's economic record by noting that median household wealth has increased on his watch. But that uptick is mostly due to home and car value inflation — meaning it's of limited use to regular people who need their home and cars to live.

President Joe Biden speaks during a meeting in the Roosevelt Room of the White House on November 21, 2023 in Washington, DC. (Drew Angerer / Getty Images)

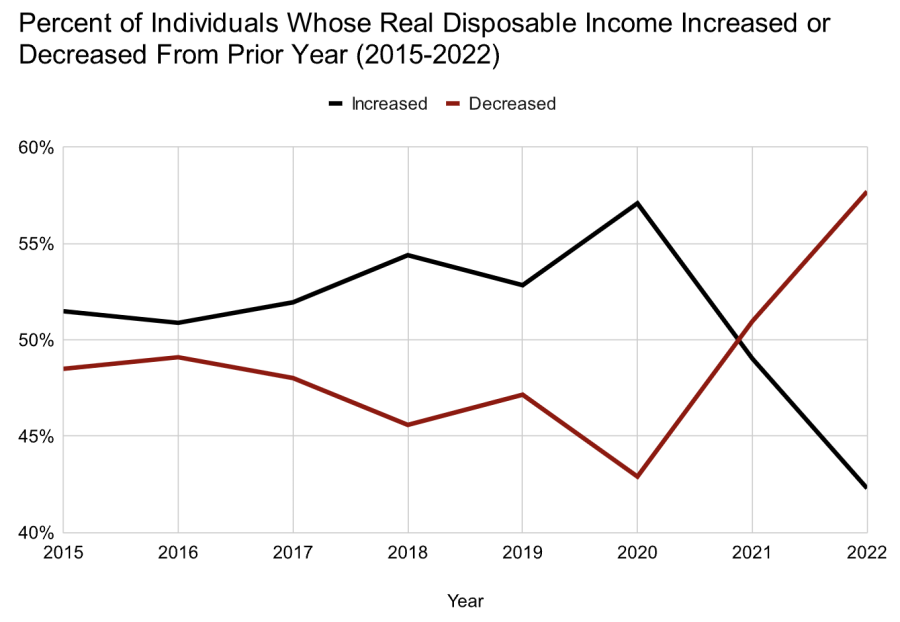

Late last month, I wrote a piece explaining why some people might say the economy under Joe Biden has not been so good. For left-wing intellectuals, Biden’s failure to reform the labor market (e.g., through the passage of the PRO Act) and his failure to reform the welfare state (e.g., through the passage of Build Back Better) provide plenty of reason for disappointment. For regular people, the unwinding of the COVID welfare state and inflation caused real incomes to decline for most.

The latter point about changes in real income generated a lot of responses.