Workers’ Pensions Are Backing Child Labor Through Private Equity Investments

Public officials have been using the retirement savings of unionized public employees to capitalize, through private equity investments, an outsourcing business that has used low-paid immigrants and even children for hazardous work in slaughterhouses.

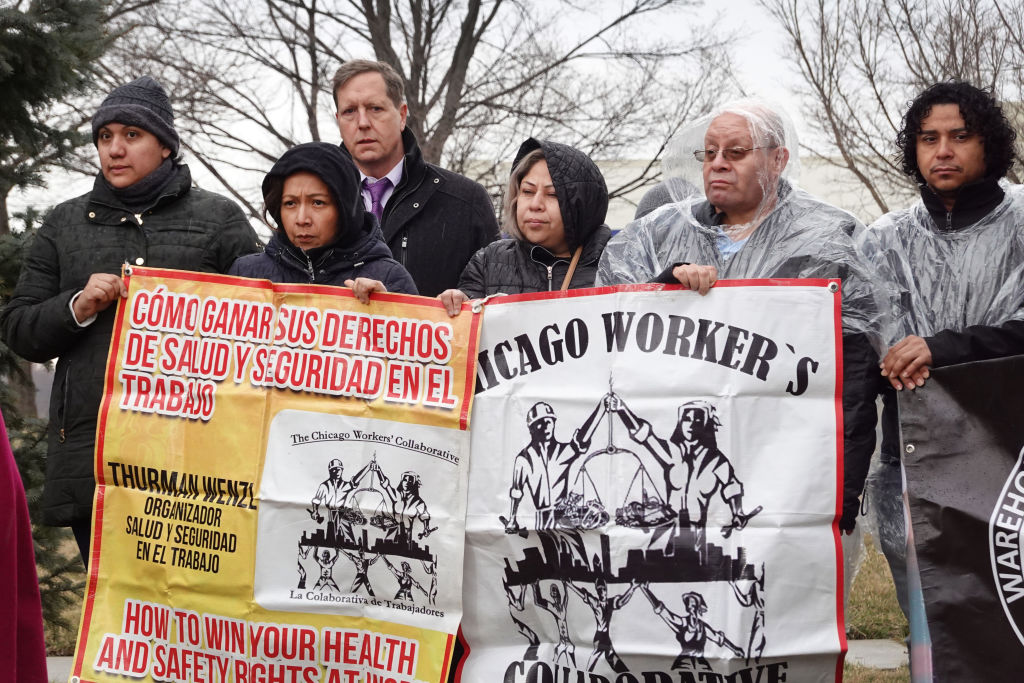

Activists gather near the Hearthside Foods packaging facility on March 6, 2023 in Bolingbrook, Illinois, protesting the employment of child workers at the facility. (Scott Olson / Getty Images)

Last month, the Biden administration announced it fined a company for employing more than a hundred children to clean meatpacking plants — one of the most dangerous jobs possible, for one of the most dangerous employers in America.

That company, a sanitation contractor called Packers Sanitation Services Inc., has been repeatedly bought and sold by private equity funds that manage retirement money for state and local public employees, according to our review.

In other words, public officials have been using the retirement savings of unionized teachers, firefighters, and police officers to capitalize — and help Wall Street executives profit from — an outsourcing business that has used low-paid immigrants and even children for hazardous work in slaughterhouses.