The Fire Next Time

Almost 60 years ago, Joan Didion wrote that “the city burning is Los Angeles’s deepest image of itself.” Since then, insurance companies and developers have prioritized short-term profits over housing resilience and affordability for Californians.

A firefighter in Oxnard, near Los Angeles, California, on January 13, 2025. (Etienne Laurent / AFP via Getty Images)

“The city burning is Los Angeles’s deepest image of itself. . . . The wind shows us how close to the edge we are.” This was Joan Didion writing in 1968 on the effect that the Santa Ana winds have had on the psyche and landscape of Southern California. Almost sixty years on, it remains an enduring image of California: a state constantly on the precipice of disaster. The precipice has only gotten closer as climate change has made the winds stronger and the landscape drier.

This year, winds, their power made worse by climate change, have again laid bare the impermanence of life between the San Gabriels and the Pacific. As of January 13, twenty-four people have lost their lives to the fires, and twenty people are still missing. About 180,000 people have been displaced, and about 12,000 structures have been destroyed. Aside from lives and structures, the Palisades and Eaton fires will have long-term consequences for public health. Particulate matter from wildfire smoke can have lasting health implications and contributes to the 100,000 people who die every year from air pollution.

It will, however, only be in the aftermath of these fires that their true toll will emerge. Those whose homes have survived may face substantial insurance claims for damages; those lucky enough to not have lost their homes will have to bear cost of skyrocketing insurance premiums; the uninsured or underinsured will have no homes to return to.

Many survivors will lack the resources to rebuild, let alone move elsewhere, because of the state’s insurance and housing affordability and availability crises. Exclusive urban planning in Los Angeles has long limited the stock of affordable housing. A flood of displaced residents from the Palisades and Eaton fires into the short-term rental market will put further pressure on an already costly housing landscape. While the LA City Council recently voted to increase housing development in already high-density residential suburbs and in areas zoned for commercial use, it did not do so for single-family zones, reinforcing a culture of low-density, exclusive development into the fire-prone suburbs.

The slower, quieter recovery crisis will take root among the residents of Los Angeles who do not live in beachside mansions. While the Palisades fire impacted wealthy households, it also ravaged manufactured homes. Altadena, a historically black and middle-income community, burned in the Eaton fire. As in many crises, media coverage and attention influence the politics of visibility. The communities seen in the eyes of FEMA, post-disaster response teams, and the East Coaster looking at GoFundMes from afar are often the ones that get to rebuild, recover, and stay. In many cases, wildfires displace working- and middle-class residents and replace them with people who can afford to rebuild.

The fires aren’t even fully extinguished in LA, yet residents are already confronting the realities of collapsing insurance markets in the state and across the country. Many articles on the LA fires and insurance coverage point to a particular statistic: months before the Palisades fire, State Farm nonrenewed nearly 70 percent of its policyholders in the Palisades. But it is not just the Pacific Palisades that will be impacted by the current fire, it’s not just Los Angeles, and it’s not just single-family homeowners.

Across the state, multifamily building owners, affordable housing providers, manufactured housing dwellers, and renters will also experience increased financial precarity from this crisis. According to research from the Consumer Federation of America, more than one-third (35 percent) of manufactured homeowners lack home insurance. There are also racial and income inequities as to who is able to afford or obtain home insurance: homeowners of color and homeowners with lower incomes are less likely to be insured. Similar patterns show up across the country.

These are issues central to all the households impacted by the LA fires, but they should also be of concern to households and policymakers across the state and the country. The availability, affordability, and resulting uptake of insurance defines the answers to many questions: Who will have to leave and who gets to stay? Will people who stay build back safer? Why do people live in those risky places to begin with? The insurance market also constrains what housing can be built in California. It affects not only the affordability of homes but also determines whether some homes can be built at all. This is because access to insurance dictates the availability and cost of mortgages, since banks are unlikely to offer mortgages to homes that can’t get insurance. For families burdened with debt, the funds provided by insurance payouts often the only way that, after a disaster like this year’s fires, they can get back on their feet.

Insurance can be thought of as a form of mutual aid, in that it pools risk across a wide population and spreads exposure to different types and levels of risk (and associated losses) across larger geographic areas so that harm from a disaster is more easily absorbed by more people sharing the risk. Because of current reliance on private insurance companies, which prioritize profit over protecting households, insurers have tried to shift away much of the risk that they take on when offering policies.

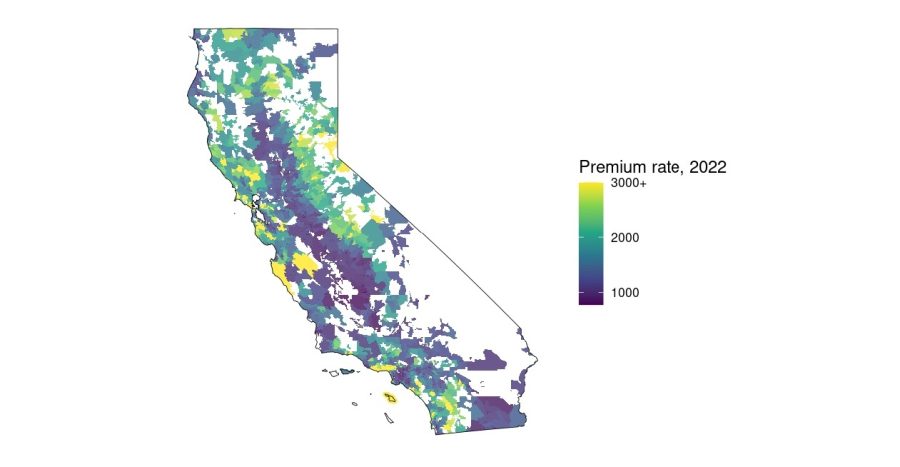

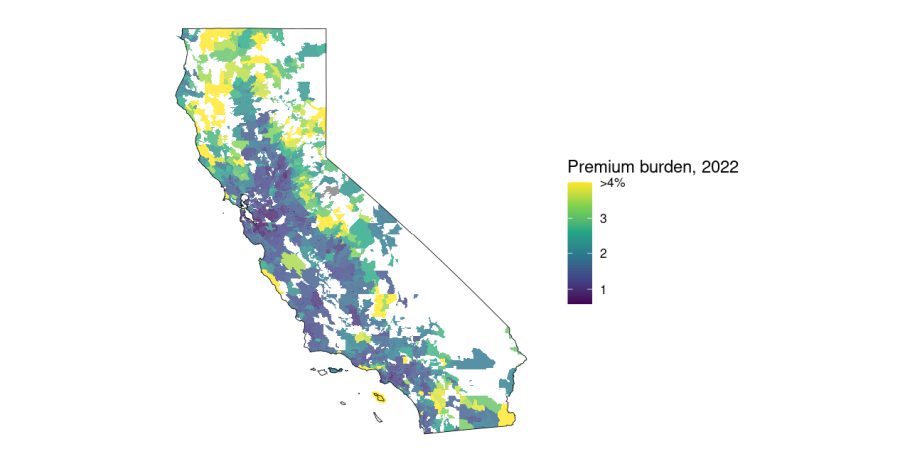

They do this in various ways, including by shifting more and more risk to policyholders, which takes the form of premium increases and coverage reductions. Research from the Climate and Community Institute that drew on insurance data from 2017 to 2022 shows that insurers have spread risk and increased premiums across many areas of California. This phenomenon has disproportionately burdened lower-income zip codes and prioritized short-term profit seeking by insurers.

The risk shifting also takes the form of placing the burden of risk reduction on policyholders, justified through what economists call “price signaling.” Price signal theory argues that increased rates (and even the availability of coverage) motivate consumers to either move out of harm’s way or pay more for that risk. Yet there are many flaws to this theory.

First, affluence is often blind to risk signaling. Second, price signaling disproportionately burdens lower-income zip codes. Instead of producing a safer outcome for those in lower-income zip codes, price signaling can increase precarity by making it more difficult to live in a certain area. Difficulty living in an area can lead to danger when there is a fundamental push and pull between affording an insurance premium and protecting one’s home through wildfire mitigation measures, which are also expensive.

Price signaling also doesn’t work well in the context of disasters like the LA fires because of its reliance on individualized risk-reduction measures. Home hardening and defensible space — ways of making homes and the surrounding landscape more fire resistant — are often regulated and considered at the parcel level. The ability to access home insurance depends largely on a suite of individual factors and produces an “every-consumer-for-themselves” mentality when insurers limit their coverage in a geographic area to avoid risk pooling and maintain profit margins.

The individualization of risk mitigation runs counter to the very essence of wildfire as a hazard. Wildfire knows no property bounds. It is inherently multijurisdictional, and its effects are felt across communities, across counties, and across states. It requires housing more people in less risky places and investing in community-scale wildfire risk reduction measures.

The reliance on private insurance markets and price signal theory also doesn’t account for the interplay between disaster risk and housing policy. California, a state with a serious housing affordability crisis, has no comprehensive land use or affordable housing policy to ensure adequate affordable housing in less risky areas. Instead, many of the remaining affordable places to live are located in areas more prone to wildfire (known as the wildland-urban interface, or WUI), and policymakers have thus far failed to stand up to a building and real estate lobby that insists on (and benefits) from expanding into the WUI.

Although the state has a semipublic system in place to respond to the insurance availability crisis, the California FAIR Plan, it is an unsustainable stop gap. Research from CCI shows that the FAIR Plan took on more and more policies from 2017 to 2022, while the private insurance market decreased its coverage throughout the state. This phenomenon has resulted in less coverage for consumers, higher costs, and a system teetering on the brink of insolvency. While private insurers limit their geographical footprints, the FAIR Plan has since taken on a high concentration of “risky” zip codes. California’s shifting insurance landscape may force wealthy residents to forgo protection of their homes, which could inadvertently lead to a massive socialization of risk when state and federal disaster relief funds grow in demand. But it could also mean poorer residents are forced out of their homes or cannot rebuild, because they cannot afford a mortgage needed for their insurance premiums.

Rather than prioritize profit, solutions must prioritize safety and affordability as disasters increase in frequency and scale. A dedicated California state housing resilience agency, which would coordinate disaster reduction activities and provide public disaster insurance, is one avenue to help us get there. An entity like this could host public catastrophe risk models, incorporate a diverse financing stream that reflects the mutuality of risk beyond the policyholder, and host a standardized pricing mechanism that ensures affordable and accessible costs for people. This agency could also lead preventative relocation efforts that guard against the production of new risky housing, ensure the construction of green social housing, and build solidarity across state lines. This kind of approach is needed across the country, because while today’s tragic disaster is in California, the next might be in Florida or Colorado or Tennessee.

The path forward is not easy, but just as winds bring change and destruction, they also make it possible to imagine new life. New life requires new systems of care and new ways of relating to each other. Some of us directly experienced the Palisades and Eaton fires, some of us know someone who did, and some of us, hundreds of miles away, will feel the impacts of the fire in an insurance premium notice, delivered in the mail on an inconspicuous Tuesday morning. Impacts of disasters are collectively felt, and it’s only reasonable that looking forward, they should be collectively mitigated.