The Child Tax Credit Can Be a Poverty-Fighting Machine

The Child Tax Credit expansion last year lifted several million children out of poverty, before Democrats failed to extend it. Now Congress is debating the policy again — and this time they have the chance to ensure even more children receive the benefit.

Eliminating the phase-in for the Child Tax Credit would reduce childhood deprivation significantly. (Alaric Sim / Unsplash)

The question of what to do with the Child Tax Credit has reared its head again, primarily due to a likely doomed push to get an expansion of it as part of extending certain corporate tax breaks. Rachel Cohen has a piece on the political wrangling over it at Vox and Matt Yglesias has a piece about what to do on the CTC over at Slow Boring.

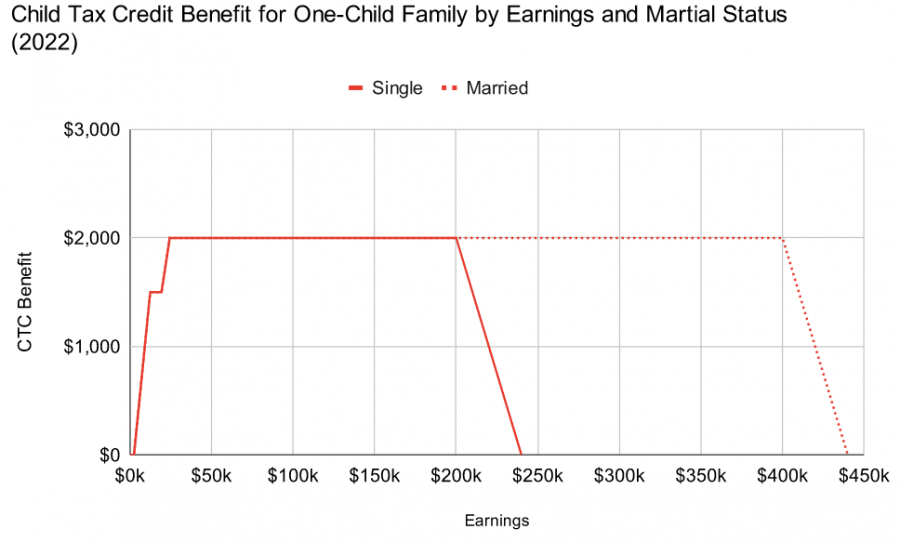

At present, the CTC looks like this.