Are Bail Bond Insurers Engaged in a Price-Fixing Conspiracy?

In California, an antitrust lawsuit is arguing that the insurance companies that underwrite bail bonds have for decades illegally colluded to keep bail bond premiums artificially high across the industry.

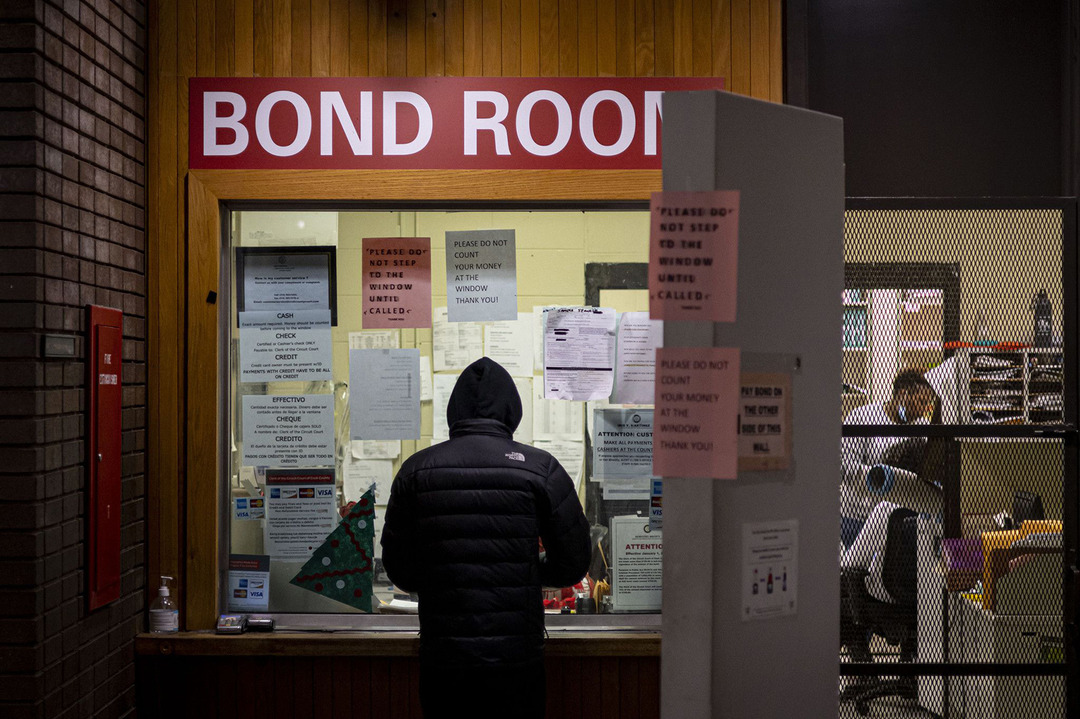

A man pays cash bail in the bond office to secure his brother’s release on December 21, 2022, at Division 5 of Cook County Jail in Chicago. (Brian Cassella / Chicago Tribune / Tribune News Service via Getty Images)

When you think of the bail industry, you’re likely to think of bail agents and their bounty hunters, who chase down fugitives released on bail for a fee, sometimes employing questionable tactics. But the true profiteers of the United States’ distinctive cash-bail system are insurance brokers, the little-known surety companies that underwrite bail bonds and often collect much of the profits.

An ongoing legal battle in California is exposing the immense power and influence of these bail surety companies, which stand accused of conspiring to keep bail bond premiums at artificially inflated rates to boost profits. If true, this means people are being fleeced trying to get themselves or a loved one out of jail — if they’re able to afford the exorbitant prices at all.

The lawsuit details how for years, the surety lobby allegedly retaliated against bail bondsmen who defected from the price-fixing scheme. According to court records, insurance executives and bail bondsmen colluded to keep bail prices sky-high at industry gatherings at resorts and in Las Vegas casinos and spread misinformation to consumers about bail rates.