Is Capitalism Terminally Ill?

A debate between Seth Ackerman and Aaron Benanav on the prognosis for capitalism: Is it experiencing the kind of long-run stagnation that many Marxists have long regarded as its destiny? And what does the answer mean for socialist political strategy today?

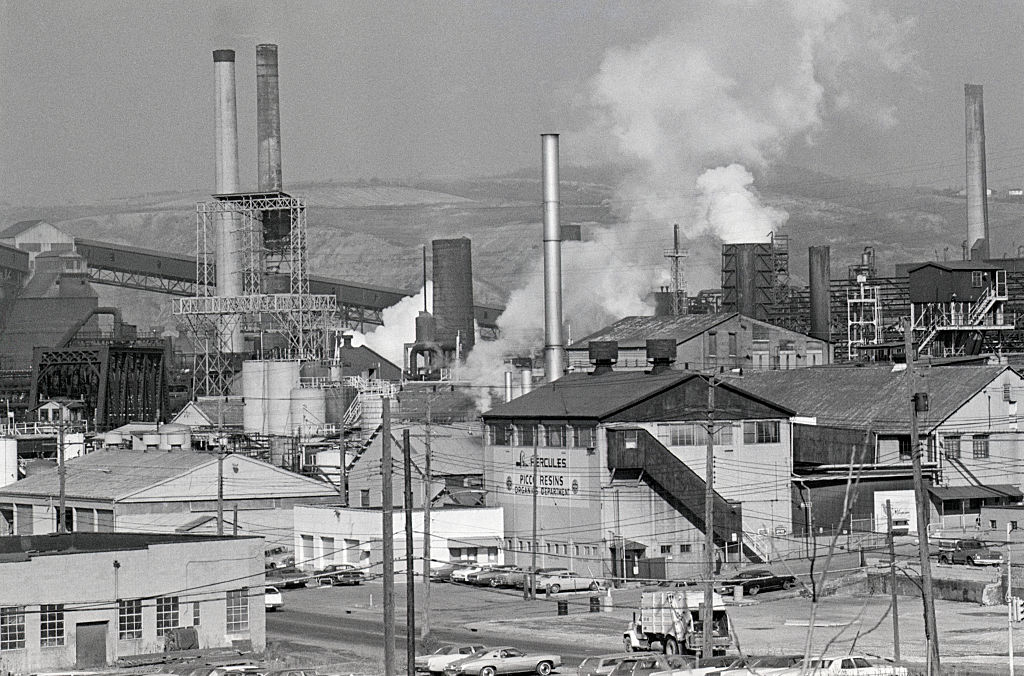

A steel mill in Pennsylvania during the 1970s, the decade when some thinkers believe capitalist growth began to stagnate. (Bettmann via Getty Images)

For the last couple of decades, New Left Review (NLR) has been publishing articles diagnosing the capitalist system as suffering from long-term stagnation, chronic overcapacity, declining profitability, and sluggish growth.

The emphasis began with a 1998 paper by the historian Robert Brenner, “The economics of global turbulence,” an article that impressed and influenced many. Brenner focused on the decline in manufacturing in particular. As Europe and Japan finally caught up to the United States, he argued, capitalist competition became something of a zero-sum game that seemed to produce mostly losers (even if a string of negatives doesn’t usually add up to zero). Other NLR contributors have continued writing variations on this theme, among them the sociologist Aaron Benanav.

In a recent article for Jacobin, Seth Ackerman filed a vigorous dissent from the line; Benanav responded shortly afterward. In what follows, Benanav and Ackerman debate the question, with me moderating. You can find an audio version of the discussion on my program, Behind the News. (Subscribe to Jacobin Radio to keep up with it.)